Which Expense Can Be Recognized in Full in March

The Importance of Timing: Revenue and Expense Recognition

Revenue is recognized when earned and payment is bodacious; expenses are recognized when incurred and the acquirement associated with the expense is recognized.

Learning Objectives

Explain how the timing of expense and revenue recognition affects the fiscal statements

Fundamental Takeaways

Fundamental Points

- According to the principle of revenue recognition, revenues are recognized in the flow earned (buyer and seller have entered into an understanding to transfer assets ) and if they are realized or realizable ( cash payment has been received or collection of payment is reasonably assured).

- The matching principle, part of accrual bookkeeping, requires that expenses be recognized when obligations are (ane) incurred (usually when goods are transferred or services rendered), and (2) that they offset recognized revenues, which were generated from those expenses.

- As long every bit the timing of the recognition of revenue and expense falls inside the same accounting period, the revenues and expenses are matched and reported on the income argument.

Fundamental Terms

- incur: To return somebody liable or subject to.

- accrual accounting: refers to the concept of recognizing and reporting revenues when earned and expenses when incurred, regardless of the effect on cash.

- matching principle: An accounting principle related to revenue and expense recognition in accrual accounting.

Revenues and Matching Expenses

According to the principle of revenue recognition, revenues are recognized in the period when it is earned (buyer and seller accept entered into an agreement to transfer assets) and realized or realizable (greenbacks payment has been received or collection of payment is reasonably assured).

For case, if a company enters into a new trading human relationship with a buyer, and it enters into an agreement to sell the buyer some of its goods. The company delivers the products merely does not receive payment until 30 days afterward the delivery. While the company had an agreement with the buyer and followed through on its end of the contract, since at that place was no pre-existing relationship with the buyer prior to the sale, a conservative accountant might not recognize the acquirement from that auction until the company receives payment 30 days later.

Expense Recognition

The assets produced and sold or services rendered to generate revenue also generate related expenses. Accounting standards require that companies using the accrual basis of bookkeeping and lucifer all expenses with their related revenues for the menstruum, and so that the income argument shows the revenues earned and expenses incurred in the correct accounting period.

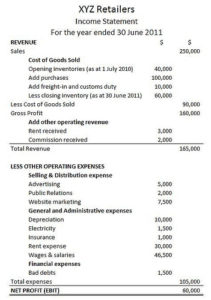

A Sample Income Argument: Expenses are listed on a company's income argument.

The matching principle, part of the accrual accounting method, requires that expenses be recognized when obligations are (1) incurred (usually when appurtenances are transferred, such as when they are sold or services rendered) and (2) the revenues that were generated from those expenses (based on cause and effect) are recognized.

For example, a visitor makes toy soldiers and acquires wood to brand its goods. Information technology acquires the woods on Jan ist and pays for it on January 15th. The wood is used to brand 100 toy soldiers, all of which are sold on Feb 15. While the costs associated with the woods were incurred and paid for during January, the expense would not be recognized until Feb 15th when the soldiers that the forest was used for were sold.

If no cause-and-upshot human relationship exists (e.g., a sale is impossible), costs are recognized as expenses in the accounting catamenia they expired (e.g., when they have been used up or consumed, spoiled, dated, related to the production of substandard goods, or the services are non in demand). Examples of costs that are expensed immediately or when used upwards include administrative costs, R&D, and prepaid service contracts over multiple bookkeeping periods.

The Effect of Timing on Revenues & Expenses

Often, a business concern will spend cash on producing their goods before it is sold or volition receive cash for skilful sit has not yet delivered. Without the matching principle and the recognition rules, a business would exist forced to record revenues and expenses when it received or paid cash. This could misconstrue a business's income statement and make it look similar they were doing much ameliorate or much worse than is really the case. By tying revenues and expenses to the completion of sales and other coin generating tasks, the income statement volition better reverberate what happened in terms of what revenue and expense generating activities during the bookkeeping period.

Electric current Guidelines for Revenue Recognition

Transactions that result in the recognition of revenue include sales avails, services rendered, and acquirement from the use of company assets.

Learning Objectives

Explain how the revenue recognition principle affects how a transaction is recorded

Key Takeaways

Key Points

- Under accrual accounting, revenues are recognized when they are realized (payment collected) or realizable (the seller has reasonable balls that payment on appurtenances will exist collected) and when they are earned (usually occurs when appurtenances are transferred or services rendered).

- For companies that don't follow accrual accounting and utilise the cash -basis instead, revenue is only recognized when cash is received.

- Revenue recognition is a part of the accrual accounting concept that determines when revenues are recognized in the accounting period.

- The matching principle, along with revenue recognition, aims to match revenues and expenses in the right accounting catamenia. It allows a improve evaluation of the income statement, which shows the revenues and expenses for an bookkeeping menstruation or how much was spent to earn the period's acquirement.

Cardinal Terms

- stock-still asset: Asset or property which cannot hands be converted into cash, such equally land, buildings, and machinery.

- intangible asset: Any valuable property of a business that does not appear on the balance sheet, including intellectual property, customer lists, and goodwill.

Revenue Recognition Concepts

The revenue recognition principle is a cornerstone of accrual bookkeeping together with the matching principle. They both decide the accounting period in which revenues and expenses are recognized. Co-ordinate to the principle, revenues are recognized if they are realized or realizable (the seller has collected payment or has reasonable assurance that payment on goods will be collected). Revenues must also exist earned (usually occurs when goods are transferred or services rendered), regardless of when greenbacks is received. For companies that don't follow accrual bookkeeping and use the cash-basis instead, acquirement is only recognized when cash is received.

Presentation of Revenue Trends over Fourth dimension: Guidelines for revenue recognition will affect how and when revenue is reported on the income statement.

Transactions that Recognize Revenue

Transactions that result in the recognition of acquirement include:

- Sales of inventory, which are typically recognized on the engagement of sale or appointment of delivery, depending on the shipping terms of the sale

- Sales of assets other than inventory, typically recognized at point of auction.

- Sales of services rendered, recognized when services are completed and billed.

- Revenue from the use of the company'southward assets such equally interest earned for money loaned out, rent for using fixed assets, and royalties for using intangible assets, such every bit a licensed trademark. Revenue is recognized due to the passage of time or as assets are used.

The Matching Principle

The matching principle's main goal is to friction match revenues and expenses in the correct bookkeeping flow. The principle allows a amend evaluation of the income statement, which shows the revenues and expenses for an accounting period or how much was spent to earn the period's acquirement. Past following the matching principle, businesses reduce confusion from a mismatch in timing betwixt when costs (expenses) are incurred and when revenue is recognized and realized.

Recognition of Revenue at Betoken of Auction or Delivery

Companies tin can recognize revenue at point of sale if it is also the date of commitment or if the buyer takes firsthand ownership of the goods.

Learning Objectives

Explain how the commitment date affects revenue recognition

Key Takeaways

Primal Points

- The accrual journal entry to record the sale involves a debit to the accounts receivable account and a credit to sales revenue; if the sale is for cash, debit cash instead. The revenue earned volition be reported as part of sales revenue in the income argument for the electric current accounting period.

- When transfer of ownership of goods sold is not immediate and delivery of the goods is required, the shipping terms of the sale dictate when revenue is recognized. Shipping terms are typically " FOB Destination" and "FOB Shipping Point".

- If a company cannot reasonably estimate the amount of future returns and/or has extremely loftier rates of returns on sales, they should recognize revenues only when the correct of return expires.

Fundamental Terms

- accrual: A charge incurred in one accounting catamenia that has not been paid by the end of it.

- FOB: Stands for "Costless on Board" or "Freight on Board"; specifies which party (buyer or seller) pays for shipment and loading costs, and/or where responsibility for the goods is transferred.

Recognizing Revenue at Indicate of Sale or Delivery

Appurtenances sold, especially retail goods, typically earn and recognize acquirement at betoken of auction, which can besides be the appointment of delivery if the buyer takes firsthand ownership of the merchandise purchased. Since almost sales are fabricated using credit rather than cash, the revenue on the sale is even so recognized if collection of payment is reasonably assured. The accrual journal entry to record the sale involves a debit to the accounts receivable account and a credit to the sales revenue account; if the sale is for cash, the greenbacks account would exist debited instead. The revenue earned will be reported as part of sales revenue in the income argument for the electric current accounting flow.

Street Market in Bharat with Appurtenances for Sale: A street market seller recognizes acquirement when he relinquishes his merchandise to a buyer and receives payment for the detail sold.

Terms of Delivery

When the transfer of buying of goods sold is non immediate and delivery of the goods is required, the shipping terms of the auction dictate when acquirement is recognized. Aircraft terms are typically "Play tricks Destination" and "FOB Shipping Point". For goods shipped nether FOB destination, ownership passes to the buyer when the goods arrive at the buyer's receiving dock; at this point, the seller has completed the sales transaction and acquirement has been earned and is recorded. If the shipping terms are Flim-flam aircraft betoken, ownership passes to the buyer when the appurtenances get out the seller'south shipping dock, thus the sale of the goods is complete and the seller can recognize the earned revenue.

Revenue Recognition & Right of Return

If a company cannot reasonably estimate the amount of futurity returns and/or has extremely high rates of returns on sales, they should recognize revenues simply when the right of return expires. Those companies that tin estimate the number of time to come returns and take a relatively minor return rate tin can recognize revenues at the point of sale, just must deduct estimated future returns.

Recognition of Acquirement Prior to Delivery

Accrual accounting allows some revenue recognition methods that recognize revenue prior to delivery or sale of appurtenances.

Learning Objectives

Distinguish betwixt the percent of completion method and the completion of product method of revenue recognition

Key Takeaways

Central Points

- For most appurtenances that take been sold and are undelivered, the sales transaction is not complete and revenue on the auction has not been earned. In this case, an accrual entry for revenue on the auction is not made.

- The cash method of accounting recognizes revenue and expenses when greenbacks is exchanged. For a seller using the greenbacks method, if cash is received prior to the delivery of goods, the cash is recorded every bit earnings.

- Under the percentage-of-completion method, if a long-term contract specifies the toll and payment options with transfer of ownership and details the heir-apparent's and seller'south expectations, then revenues, costs, and gross profit can be recognized each flow based upon the progress of construction.

- The completion of production method allows recognizing revenues even if no sale was fabricated. This applies to natural resource where in that location is a ready market place for these products with reasonably assured prices, units are interchangeable, and selling and distributing costs are not pregnant.

Cardinal Terms

- conservatism: A chance-averse mental attitude or approach; for accounting purposes, it relates to disclosing expenses and losses incurred immediately and delaying the recognition of revenues and gains until realized.

- accrual: A accuse incurred in one accounting period that has non been paid by the finish of it.

Definition of Acquirement Recognition

The accounting principle regarding revenue recognition states that revenues are recognized when they are earned (transfer of value between buyer and seller has occurred) and realized or realizable (collection is reasonably bodacious). A transfer of value takes place between a buyer and seller when the buyer receives appurtenances in accordance to a sales order approved by the buyer and seller and the seller receives payment or a hope to pay from the buyer for the appurtenances purchased. Revenue must be realizable. In order words, for sales where cash was non received, the seller should be confident that the heir-apparent volition pay co-ordinate to the terms of the sale.

Goods in Inventory: Depending on the aircraft terms of the sale, a seller may not recognize revenue on goods sold that are pending delivery.

Methods that Recognize Revenue Prior to Delivery or Sale

- Percent-of-completion method: if a long-term contract clearly specifies the price and payment options with transfer of ownership — the buyer is expected to pay the whole amount and the seller is expected to complete the project — and then revenues, expenses, and gross turn a profit tin be recognized each period based upon the progress of construction (that is, percentage of completion). For case, if during the twelvemonth, 25% of the building was completed, the architect can recognize 25% of the expected total profit on the contract. Percent of completion is preferred over the completed contract method. However, expected loss should be recognized fully and immediately due to the conservatism constraint. All revenues, expenses, losses, and gains resulting from the percentage completed will be reported on the income statement.

- Completion of product method: This method allows recognizing revenues even if no auction was made. This applies to agricultural products and minerals because there is a ready market for these products with reasonably assured prices, the units are interchangeable, and selling and distributing does not involve significant costs. All expected revenues and costs of production related to the units produced volition be reported on the income statement.

Recognition of Revenue Later Delivery

There are three methods that recognize revenue subsequently delivery has taken place: the installment sales, cost recovery, and deposit methods.

Learning Objectives

Differentiate betwixt the installment sales method, the cost recover method and the deposit method to account for recognizing revenue later the delivery of goods

Key Takeaways

Key Points

- When a sale of goods carries a high incertitude on collectibility, a company must defer the recognition of revenue until after commitment.

- The installment sales method recognizes income after a sale or commitment is fabricated; the revenue recognized is a proportion or the production of the percentage of acquirement earned and cash collected.

- The cost recovery method is used when at that place is an extremely high probability of uncollectable payments. Nether this method, no acquirement is recognized until greenbacks collections exceed the seller's cost of the merchandise sold.

- The deposit method is used when a company receives greenbacks before transfer of ownership occurs. Revenue is non recognized when cash is received, because the risks and rewards of ownership have not transferred to the buyer. Only as the transfer of value takes place is revenue recognized.

Fundamental Terms

- deferral: An business relationship where the asset or liability recording greenbacks paid or received is not realized until a future date (accounting period)

- liability: An obligation, debt or responsibility owed to someone.

Recognizing Revenue after Commitment of Goods

When a sale of goods transaction carries a high degree of uncertainty regarding collectibility, a company must defer the recognition of acquirement. In this state of affairs, revenue is not recognized at signal of auction or commitment. There are three methods that recognize revenue after delivery has taken place:.

Service Delivery: Delivery of appurtenances or service may not be enough to allow for a business organization to recognize acquirement on a auction if there is doubt that the customer volition pay what it owes.

The installment sales method recognizes income after a sale or delivery is made; the acquirement recognized is a proportion or the product of the percentage of revenue earned and cash collected. The unearned income is deferred (recorded equally a liability ) and and so recognized to income when cash is collected. For instance, if a company nerveless 45% of a production'south sale price, it can recognize 45% of total revenue on that product. The installment sales method is typically used to business relationship for sales of consumer durables, retail country sales, and retirement property.

The cost recovery method is used when there is an extremely high probability of uncollectable payments. Under this method, no acquirement is recognized until cash collections exceed the seller's cost of the merchandise sold. For case, if a company sold a machine worth $x,000 for $15,000, it tin can start recognizing revenue when the heir-apparent has fabricated payments in backlog of $10,000. In other words, each dollar collected greater than $10,000 goes towards the seller's anticipated revenue on the auction of $5,000.

The deposit method is used when a company receives cash before transfer of ownership occurs. Acquirement is not recognized when cash is received because the risks and rewards of ownership accept not transferred to the heir-apparent. The seller records the cash deposit as a deferred revenue, which is reported as a liability on the residual canvass until the revenue is earned. For instance, sales of magazine subscriptions utilize the deposit method to recognize revenue. A deferral is recorded when a seller receives a subscriber's payment on the subscription; greenbacks is debited and deferred magazine subscriptions (a liability account) is credited. As the delivery of the magazines accept place, a portion of revenue is recognized, and the deferred liability account is reduced for the amount of the revenue.

Differences Betwixt Accrual-Basis and Cash-Basis Bookkeeping

Accrual accounting does not record revenues and expenses based on the exchange of cash, while the cash-basis method does.

Learning Objectives

Differentiate between accrual and cash basis accounting

Fundamental Takeaways

Cardinal Points

- Accrual accounting does non consider cash when recording revenue; in well-nigh cases, goods must be transferred to the buyer in order to recognize earnings on the sale. An accrual journal entry is fabricated to record the revenue on the transferred appurtenances every bit long as drove of payment is expected.

- In accrual bookkeeping, expenses incurred in the same flow that revenues are earned are also accrued for with a journal entry. Same every bit revenues, the recording of the expense is unrelated to the payment of cash.

- For a seller using the cash method, revenue on the auction is not recognized until payment is collected and expenses are not recorded until cash is paid.

- The greenbacks model is only acceptable for smaller businesses for which a majority of transactions occur in cash and the use of credit is minimal.

Primal Terms

- accrue: To increase, to augment; to come to past way of increase; to ascend or spring as a growth or result; to be added as increase, profit, or impairment, especially every bit the produce of coin lent.

- liability: An obligation, debt or responsibility owed to someone.

Definition of Accrual Accounting

Under the accrual accounting method, the receipt of cash is not considered when recording acquirement; even so, in most cases, goods must exist transferred to the buyer in order to recognize earnings on the auction. An accrual journal entry is fabricated to record the revenue on the transferred goods even if payment has not been made. If goods are sold and remain undelivered, the sales transaction is not complete and revenue on the sale has non been earned. In this instance, an accrual entry for revenue on the sale is non fabricated until the goods are delivered or are in transit. Expenses incurred in the same catamenia in which revenues are earned are also accrued for with a journal entry. Just similar revenues, the recording of the expense is unrelated to the payment of cash. An expense account is debited and a cash or liability business relationship is credited.

Definition of Cash-Ground Accounting

The greenbacks method of accounting recognizes acquirement and expenses when cash is exchanged. For a seller using the greenbacks method, revenue on the auction is not recognized until payment is collected. Just like revenues, expenses are recognized and recorded when cash is paid. The Fiscal Accounting Standards Board (FASB), which dictates accounting standards for most companies—especially publicly traded companies—discourages businesses from using the cash model because revenues and expenses are non properly matched. The cash model is acceptable for smaller businesses for which a majority of transactions occur in cash and the utilize of credit is minimal. For example, a landscape gardener with clients that pay past greenbacks or check could use the greenbacks method to account for her business' transactions.

A cashier at a hotel in Thailand: The cash-basis method, unlike the accrual method, relies on the receipt and payment of cash to recognize revenues and expenses.

hooverconesee1936.blogspot.com

Source: https://courses.lumenlearning.com/boundless-accounting/chapter/revenue-recognition/

0 Response to "Which Expense Can Be Recognized in Full in March"

Post a Comment